SEC Proposes Rule to Streamline Filer Status Categories and Expand Disclosure Accommodations Available to Certain Public Companies

May 22, 2026

On May 19, 2026, the Securities and Exchange Commission (the SEC) released its proposed rule on Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies (the Proposed Rule) that, if adopted, would, among other things, make many of the scaled disclosures currently available to smaller reporting companies (SRCs) and emerging growth companies (EGCs) available to a broader group of filers. The Proposed Rule would also simplify the existing filer category framework and increase the thresholds for public companies to qualify as large accelerated filers (the category of filers that do not receive any disclosure timing or content accommodations).

Background

Over time, the SEC has offered accommodations for the timing of and disclosure content for periodic reporting to public company filers under the Securities Exchange Act of 1934, as amended (the Exchange Act), based on the company’s “filer status.” The SEC has established five partially overlapping filer statuses, each based on some combination of factors, including the company’s public float, annual revenue, and time since the company has been subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act, among others.

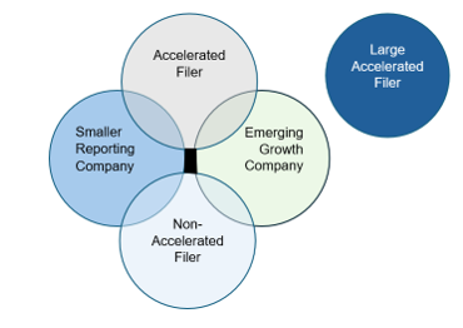

Overlap Between Current SEC Filer Status Categories

Large Accelerated Filers (LAFs), which are currently defined as filers with a public float equal to or greater than $700 million and who have been subject to the SEC’s periodic reporting requirements for more than 12 consecutive calendar months, do not receive any timing or disclosure content accommodations. Each of the other filer categories currently receive various accommodations under the SEC rules, including, but not limited to:

- Longer periods of time to file periodic reports for Accelerated Filers (AFs) and Non-Accelerated Filers (NAFs);

- Exemption from the requirement to provide auditor attestation for NAFs; and

- Scaled disclosure requirements for EGCs and SRCs (which only partially overlap, meaning scaled disclosures for an EGC-only company are not entirely the same as those provided to an SRC-only company).

The current SEC Commissioners have criticized the complexity and confusion arising from the overlapping filer categories and differing accommodations afforded to each. For example, in February 2025, SEC Commissioner Mark T. Uyeda highlighted the “complexity and compliance costs” arising out of the framework and the potential inconsistencies in their application across similarly situated smaller public companies.1 Commissioner Uyeda also criticized the thresholds for determining whether a public company qualifies as an LAF, which have remained unchanged since 2005 and which have resulted in a doubling of the percentage of public companies qualifying as LAFs since that time.2

In his statement accompanying the Proposed Rule, SEC Chair Paul S. Atkins wrote that the Proposed Rule furthers his oft-stated goal of “incentivizing smaller companies to go and stay public.”3

SEC Commissioner Hester M. Peirce, who previously questioned whether the SEC “can do more to scale disclosures across” the various filer categories,4 praised the Proposed Rule as “a positive step toward right-sizing the regulatory burden of being a public company.”5

The Proposed Rule

Changes to the Way Filer Status Is Calculated and How Companies Transition In and Out of Filer Statuses

Under current SEC rules, public companies are required to determine their filer status at the end of each fiscal year with any changes to filer status applying to the company’s filings in the immediately succeeding fiscal year (except for companies qualifying as SRCs, for which a different compliance timeline applies). When public float is a part of the filer status calculation, it is calculated as of the end of the company’s second fiscal quarter.

Under the Proposed Rule:

- public float would be calculated based on the company’s average public float over the last 10 trading days of the second quarter of the company’s fiscal year;6 and

- a company would only transition in or out of a filer status if the company has been above or below the public float threshold for two consecutive years.

By requiring that the public float threshold be met (or not met) for two consecutive years before any change to a company’s filer status, the Proposed Rule intends to (i) ensure that changes to a company’s filer status will only be made if its public float is consistently above (or below) the required threshold and (ii) give the company and the public at least one year of notice regarding the possibility of a future filer status transition before that transition could occur.

Changes to the Thresholds for LAF Status

The Proposed Rule would increase the public float and seasoning thresholds for a company to fall within the definition of LAF.

|

|

Current Rules |

Proposed Rule |

|

Public Float Threshold |

Public float of $700 million or more as of the last business day of the most recently completed second fiscal quarter |

Public float of $2 billion or more based on the average stock price over the last 10 trading days of the second fiscal quarter |

|

Seasoning Requirement |

Requires at least 12 consecutive calendar months of SEC periodic reporting before a company can become an LAF |

Requires at least 60 consecutive calendar months of SEC periodic reporting before a company can become an LAF |

The SEC estimates that the Proposed Rule would reduce the percentage of registrants that qualify as LAFs from 35% to 19%.

Extension of Disclosure Accommodations

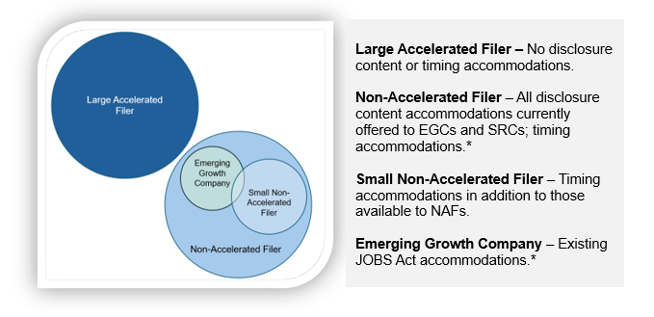

The Proposed Rule would extend all of the disclosure accommodations currently available to SRCs and EGCs to all filers other than LAFs and would streamline the filer status categories to remove SRC and AF filer categories (which will no longer have distinct applications following these changes).

- Extension of Disclosure Accommodations to All Filers Other Than LAFs. The Proposed Rule would extend the disclosure accommodations currently available to SRCs and EGCs—including the exemption from providing an auditor attestation—to all filers other than LAFs.7

- Removal of Accelerated Filer (AF) Filer Status. Because all filers that are not LAFs are treated the same under the Proposed Rule, the Proposed Rule would remove the filer status category of “Accelerated Filer.” All filers that are not LAFs are referred to as NAFs under the Proposed Rule.

- Removal of SRC Filer Status. Because the Proposed Rule gives all NAFs the benefit of disclosure accommodations currently available to EGCs and SRCs, the Proposed Rule also removes “Smaller Reporting Company” as a separate filer status. Of note, because the EGC filer status was created by and is defined in the JOBS Act, it cannot be eliminated via SEC rulemaking.

Following the changes to filer status categories in the Proposed Rule, the various filer status categories would look like this:

* The SEC staff notes in the Proposed Rule that by “proposing to permit NAFs to apply the disclosure requirements that currently apply to EGCs, [the Proposed Rule] would practically make reliance on EGC status unnecessary in most circumstances.”8

Overlap Between Proposed SEC Filer Status Categories

Additional Timing Accommodations for the Smallest NAFs

As indicated above, the Proposed Rule would create a new sub-category of NAFs called Small Non-Accelerated Filers, or SNFs, which are defined as NAFs that “report total assets of $35 million or less in [their] financial statements as of the end of each of [their] two most recent second fiscal quarters.” The two-year measurement period for transitioning in and out of SNF status mirrors the changes made to the LAF calculation under the Proposed Rule.

SNFs would be granted additional time to file their periodic reports as compared to NAFs and LAFs.

|

|

LAFs |

NAFs |

SNFs |

|

Form 10-K due… |

60 days after fiscal year end |

90 days after fiscal year end |

120 days after fiscal year end |

|

Form 10-Q due… |

40 days after fiscal quarter end |

45 days after fiscal quarter end |

50 days after fiscal quarter end |

The SEC estimates that approximately 22% of NAFs and 18% of all registrants would qualify as SNFs.

Exception to the Rollback of Disclosure Requirements: Disclosure of Unresolved Staff Comments.

The Proposed Rule would require all filers (including NAFs) to provide disclosure regarding any material unresolved comments received from SEC staff on their periodic or current reports pursuant to Item 1B of Form 10-K (Unresolved Staff Comments). Under the current SEC rules, NAFs are not required to provide this disclosure.

Next Steps

The SEC is seeking comment on, among other things:

- whether public float is a reasonable indicator of the most significant need for more extensive public disclosure, and if any alternative indicators should be used instead;

- whether the adjustments made to the $2 billion LAF public float and 60-month seasoning thresholds are appropriate, and if the SEC should adopt any alternative thresholds;

- whether the SEC should establish a mechanism to update the proposed $2 billion public float threshold;

- whether the proposed two-year period during which a filer’s status cannot change will have the intended effect of “providing registrants and investors with some consistency and predictability as to the disclosure and other requirements” to which a registrant is subject; and

- whether the SEC should extend SRC and/or EGC accommodations to all NAFs, as proposed, or whether certain categories of NAFs (for example, banks and other financial institutions) should continue to comply with certain disclosure requirements otherwise applicable only to LAFs

Comments on the Proposed Rule are due on or before July 20, 2026.

1 Mark T. Uyeda, Comm’r, Sec. & Exch. Comm’n, Remarks at the Florida Bar’s 41st Annual Federal Securities Institute and M&A Conference (Feb. 24, 2025), https://www.sec.gov/newsroom/speeches-statements/uyeda-remarks-florida-bar-022425 (pointing out that SRCs that qualify as AFs have to provide an auditor attestation, while SRCs that qualify as NAFs do not).

2 Id.

3 Paul S. Atkins, Chair, Sec. & Exch. Comm’n, Statement on Proposing Releases for Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies, and Registered Offering Reform (May 19, 2026), https://www.sec.gov/newsroom/speeches-statements/atkins-statement-on-proposing-releases-for-enhancement-of-emerging-growth-company-accommodations-and-simplification-of-filer-status-for-reporting-companies-and-registered-offering-reform-051926.

4 Hester M. Peirce, Comm’r, Sec. & Exch. Comm’n, Bridging the Gap: Remarks before the Northwest Securities Institute (May 30, 2025), https://www.sec.gov/newsroom/speeches-statements/peirce-remarks-northwest-securities-institute-053025.

5 Hester M. Peirce, Comm’r, Sec. & Exch. Comm’n, Headache Medicine: Statement on Proposing Releases for Registered Offering Reform and Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies (May 19, 2026), https://www.sec.gov/newsroom/speeches-statements/peirce-statement-proposing-releases-ror-051926.

6 If the SEC’s proposed rule on semiannual reporting is approved, companies that adopt semiannual reporting would determine public float over the last 10 trading days of the first semiannual period. The SEC’s proposed rule on semiannual reporting is discussed further in our recent Client Alert.

7 NAFs would also be accorded the option to irrevocably elect to defer compliance with new or revised financial accounting standards issued by the Financial Accounting Standards Board (an accommodation currently only available to EGCs) for their first five years after initial registration with the SEC.

8 Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies, Securities Act Release No. 11,419, Exchange Act Release No. 105,515, 91 Fed. Reg. 30086, 30097 n.124 (proposed May 19, 2026) (“EGC filer status was created by the JOBS Act. As this is a statutory status, the Commission is not proposing to eliminate the EGC filer status. We are proposing to permit NAFs to apply the disclosure requirements that currently apply to EGCs, which we believe would practically make reliance on EGC status unnecessary in most circumstances.”).

This memorandum is a summary for general information and discussion only and may be considered an advertisement for certain purposes. It is not a full analysis of the matters presented, may not be relied upon as legal advice, and does not purport to represent the views of our clients or the Firm. Shelly Heyduk, an O’Melveny partner licensed to practice law in California; Rob Plesnarski, an O’Melveny partner licensed to practice law in the District of Columbia; Andra Troy, an O’Melveny partner licensed to practice law in New York; Ashley Gust, an O’Melveny counsel licensed to practice law in New York; Aliza Cohen, an O’Melveny resource attorney licensed to practice law in California; Chloe Keedy, an O’Melveny associate licensed to practice law in California; and Kate Jones, an O’Melveny associate licensed to practice law in California, contributed to the content of this newsletter. The views expressed in this newsletter are the views of the authors except as otherwise noted.

© 2026 O’Melveny & Myers LLP. All Rights Reserved. Portions of this communication may contain attorney advertising. Prior results do not guarantee a similar outcome. Please direct all inquiries regarding New York’s Rules of Professional Conduct to O’Melveny & Myers LLP, 1301 Avenue of the Americas, Suite 1700, New York, NY, 10019, T: +1 212 326 2000.